Hunt: Households face ‘very tough’ times as mortgage costs soar

Chancellor Jeremy Hunt insisted the Government was fixing the economic difficulties caused by predecessor Kwasi Kwarteng’s mini-budget.

Jeremy Hunt has warned families will face “very tough” times as mortgage costs soar but insisted he was clearing up the economic mess left by the Liz Truss mini-budget fiasco.

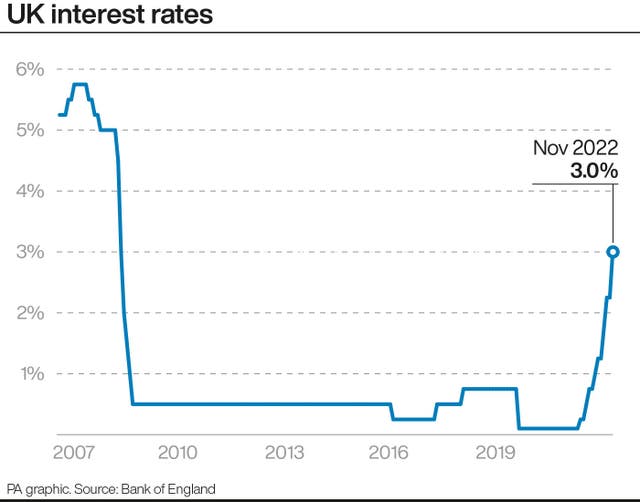

The Chancellor acknowledged the difficulties facing homeowners and businesses after the Bank of England put up its base rate from 2.25% to 3%, the highest for 14 years, and warned of a prolonged recession.

He said there were problems affecting economies around the world but in the UK Prime Minister Rishi Sunak would “fix” the issues caused by Ms Truss and former chancellor Kwasi Kwarteng in September’s financial statement.

Bank of England governor Andrew Bailey said Ms Truss’s economic policies would have a long-lasting impact, pushing up borrowing costs.

Asked whether Tory incompetence was to blame for the country’s economic problems, Mr Hunt said: “What my party has done is put in place a new Prime Minister.

“We also have a new Chancellor of the Exchequer.”

Mr Hunt said the Prime Minister recognised the problem when he entered Downing Street and said “he was there to fix that” while the Chancellor said he had reversed the measures in the mini-budget within days of entering No 11.

Mr Bailey said the Trussonomics policies of borrowing to fund tax cuts, on top of a massive spending commitment to control energy bills, would have a lasting impact on the UK’s credibility.

“There has been a questioning of UK policy,” he said. “That will have some lasting effect and we have to work very hard to put that in the past, frankly.”

He added: “There has been a UK premium on rates. If you look at how UK rates have moved since we were here at the beginning of August compared to the euro area and the US, they’ve all gone up, but the UK clearly went up far more, and it went up during this period when there was considerable turmoil in the markets.”

The increase in interest rates will pile around £3,000 per year on mortgage bills for households set to renew their home loans.

Mr Hunt said: “Today’s news is going to be very tough for families with mortgages up and down the country, for businesses with loans.

“But there is a global economic crisis, the International Monetary Fund says a third of the world’s economy is now in recession.”

Mr Hunt warned there were “no easy options” for the Government as it sought to get the national finances back under control.

Speaking to reporters in Carshalton, south London, he said: “The best thing the Government can do if we want to bring down these rises in interest rates is to show that we are bringing down our debt.

“Families up and down the country have to balance their accounts at home and we must do the same as a government.”

The Chancellor is expected to set out a package of tax rises and spending cuts in his November 17 autumn statement.

“Sound money and a stable economy are the best ways to deliver lower mortgage rates, more jobs and long-term growth.

“However, there are no easy options and we will need to take difficult decisions on tax and spending to get there.”